3.4 Control account

Understanding the Purpose of Control Accounts

What are Control Accounts?

An account that enables a business to check the arithmetical accuracy of entries posted to its ledger

Control accounts act as summary accounts that gather all the details from smaller individual accounts into one big picture. This makes it easier to see the overall amounts at a glance.

Examples of control accounts include:

Purchases Ledger Control Account (PLCA) sometimes called The Trade Payable ledger control account, which summarizes the individual suppliers’ accounts, i.e. creditors’ accounts.

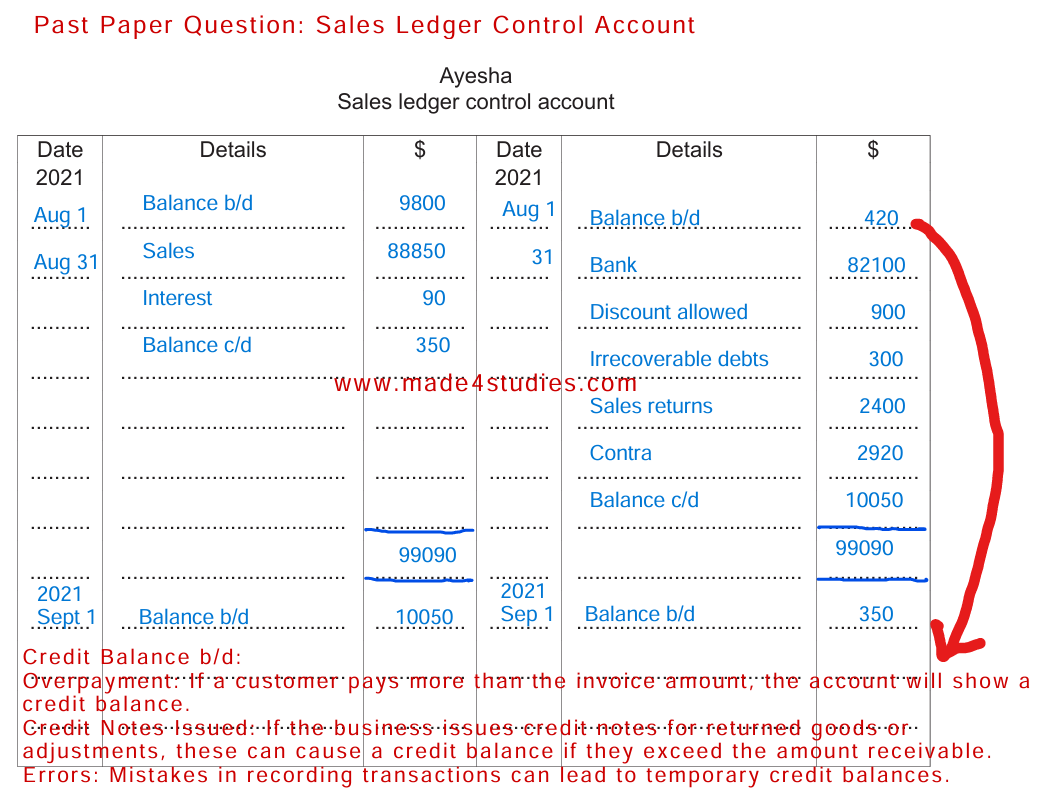

Sales Ledger Control Account (SLCA): sometimes called The Trade Receivable Ledger Control Account, which summarizes the individual customer accounts, i.e. debtors’ accounts.

identify the books of prime entry as sources of information for the control account entries

How is a contra entry treated in the control ledger accounts?

A balance on a purchase ledger account is transferred to an account for the same business in the sales ledger. The purchase ledger control account is debited, and the sales ledger control account is credited

Why Sometimes Balance b/d is on Debit Side of Purchases Ledger Control Account and Credit Side of Sales Ledger Control Account