3.3 Bank reconciliation

Bank Statement: a statement issued by the bank to show the balance in a bank account

and the amounts that have been paid into it and withdrawn from it.

Or

A Bank Statement is a summary of financial transactions occurring over a certain period on a bank account held by a business or individual.

Uses of Bank Statement?

Check for Accuracy: By comparing your bank statement to your own records (like a cash book), you can make sure everything matches up.

Manage Cash Flow: It helps you keep track of how much money is coming in and going out, so you don’t run out of cash.

Spot Mistakes: You can see if there are any errors or unauthorized transactions.

Proof of Transactions: It’s a legal record that can verify your financial activities if needed.

The Purpose of a Bank Statement

Transparency: It provides a clear and honest record of your financial transactions.

Financial Planning: It helps you plan and budget by showing you exactly where your money goes.

Audit Trail: It’s an important document for accountants and auditors to trace financial activities and ensure everything is recorded properly.

Example Question and Answer from Past Papers

Question: Why is it important for a business to regularly compare its cash book with its bank statement?

Answer:

Ensure Accuracy: Regular comparison helps make sure that the entries in the cash book are accurate and match with the bank’s records.

Find Differences: It helps spot differences, like bank charges not yet recorded, or errors in recording transactions.

Detect Fraud: Regular reconciliation can reveal any unauthorized or fraudulent transactions.

Update Records: It ensures that all bank transactions, including automatic payments like direct debits, are recorded in the cash book.

Better Control: Helps in maintaining control over finances and making better financial decisions.

unpresented cheque: a cheque that has not yet cleared through the bank system.

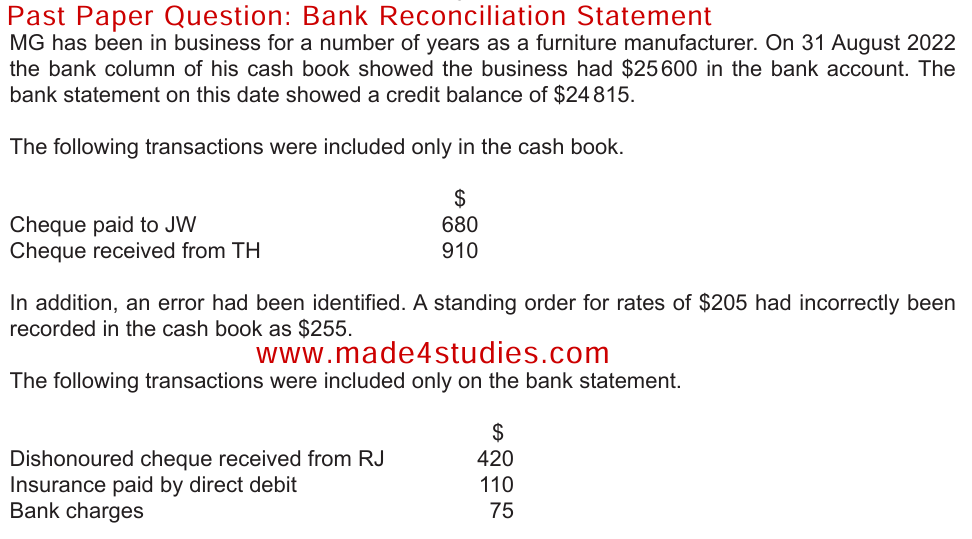

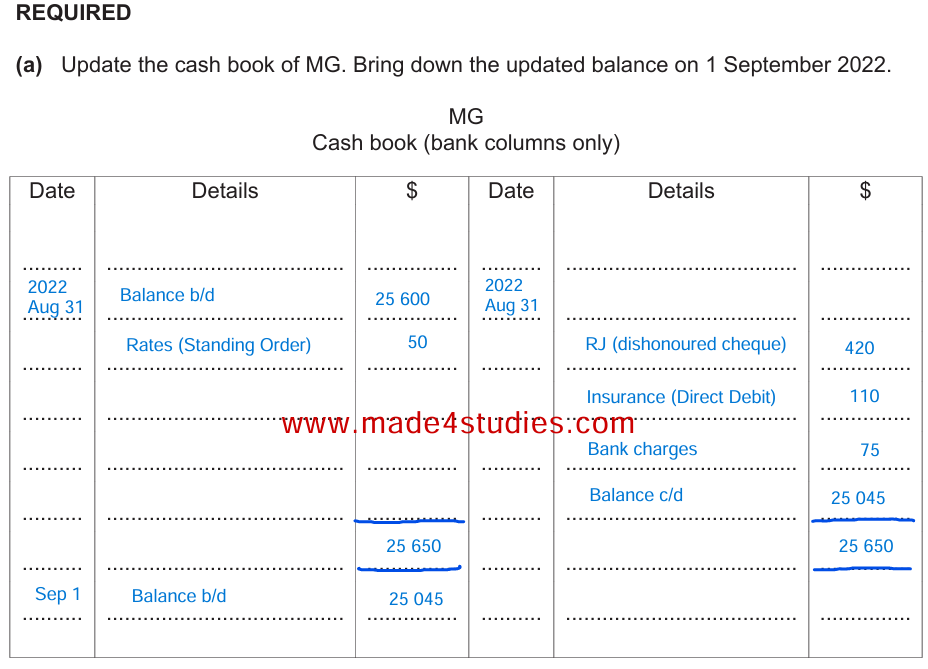

• update the cash book for bank charges, bank interest paid and received, correction of errors, credit transfers, direct debits, dividends, and standing orders

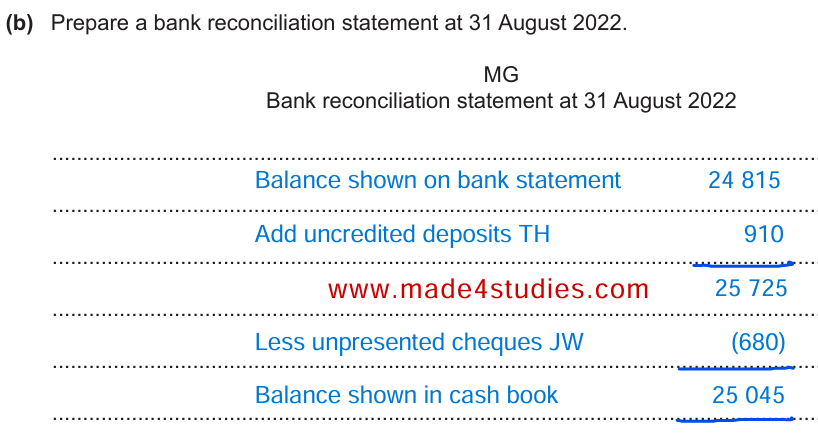

• understand the purpose of and prepare a bank reconciliation statement to include bank errors,

uncredited deposits and unpresented cheques.

Bank Reconciliation Statement: a statement comparing the cash book balance with the

bank statement balance

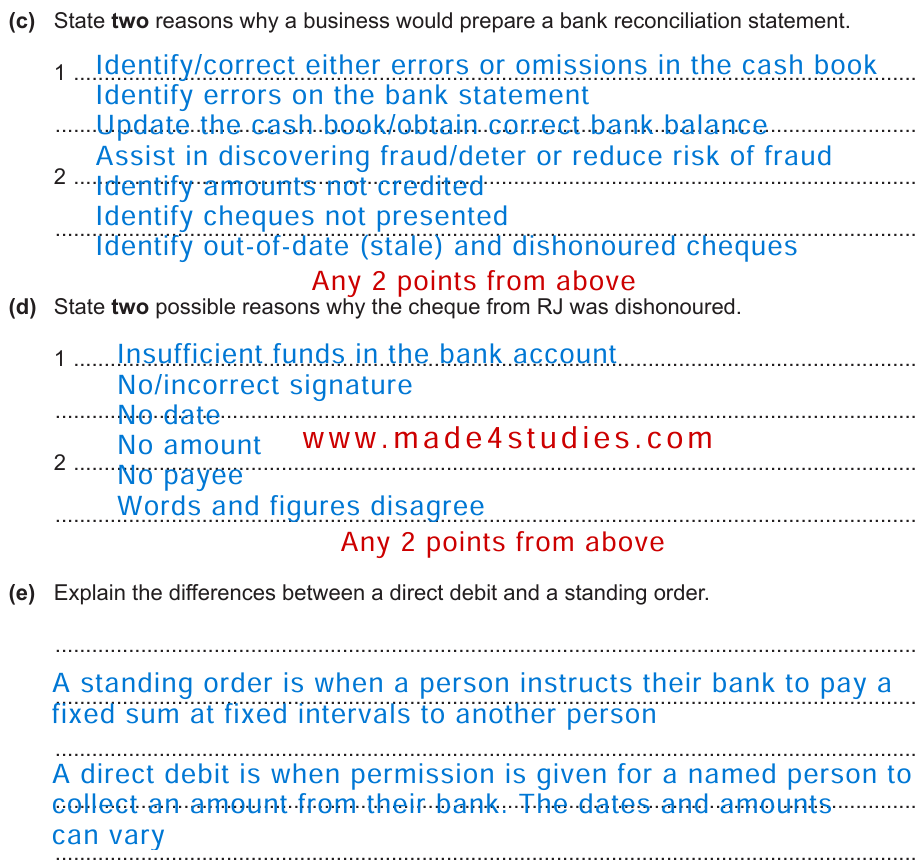

Purpose of a Bank Reconciliation Statement:

Accuracy: Ensures your cash book and bank statement match up.

Error Detection: Spots mistakes or missing entries in either the cash book or the bank statement.

Fraud Prevention: Identifies unauthorized transactions and helps prevent fraud.

Up-to-Date Records: Keeps your financial records accurate and current.

Key Terms:

Bank Errors: Mistakes made by the bank in recording transactions.

Uncredited Deposits: Deposits you’ve made but the bank hasn’t processed yet.

Unpresented Cheques: Cheques you’ve written but the bank hasn’t cashed yet.

Steps to Prepare a Bank Reconciliation Statement

Example Question and Answer from Past Papers

Question: On 31 December, the bank statement of a business showed a balance of $2,000. The cash book showed a balance of $2,500. Upon investigation, the following were found:

A cheque of $300 issued to a supplier had not been presented.

A deposit of $800 was not credited by the bank.

The bank had debited a cheque of $200 by mistake.

Prepare a bank reconciliation statement.

Answer:

Bank Reconciliation Statement as at 31 December

Adjusted Cash Book Balance: $2,500

The adjusted bank balance doesn't match the cash book balance, which means there are still differences that need to be reviewed.

.