4.1 Capital and revenue expenditure and receipts

|

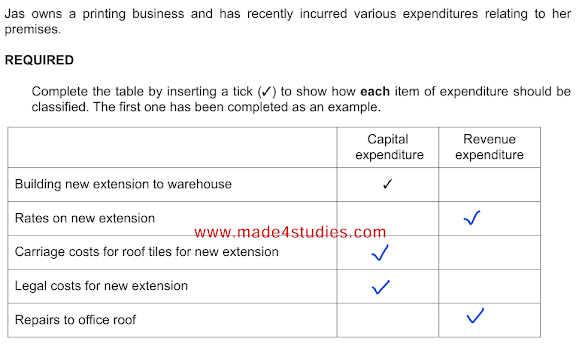

Capital Expenditure Definition: Money spent on acquiring or improving long-term assets like buildings, machinery, or equipment. These assets benefit the business over several years. |

Revenue Expenditure Definition: Money spent on the day-to-day running of the business, maintaining assets, or generating revenue in the current period. |

|

Examples: -Premises purchased -Legal charges for conveyancing New machinery -Installation of machinery Additions to assets -Motor van -Delivery charges on new assets -Extension costs of new offices -Cost of adding air-conditioning to offices |

Examples: -Rent of premises -Legal charges for debt collection -Maintenance of assets -Repairs to van -Carriage on purchases and revenue -Redecorating existing offices -Interest on loan to purchase air-conditioning |

|

It is recorded as assets on the Statement of financial position and depreciated over their useful life. |

It is recorded as expenses on the statement of profit or loss (income statement), reducing the profit for the year.. |

|

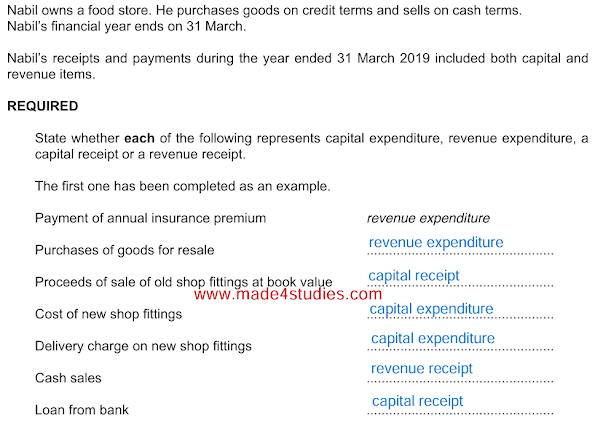

Capital Receipts Definition: Income from non-operational activities, such as selling long-term assets or receiving loan proceeds. |

Revenue Receipts Definition: Income from regular business activities. |

|

Examples: Proceeds from selling a building, obtaining a bank loan. |

Examples: Sales revenue, service fees, interest income. |

|

Not recorded as revenue; affects the SOFP (balance sheet) by increasing assets or reducing liabilities. |

Recorded as revenue on the SOPL (income statement), contributing to the net profit. |

Effects on profit when capital expenditure incorrectly treated as revenue expenditure:

Immediate Impact: Overstates expenses, understates profit.

Long-term Impact:

Reduces taxable profit in the current period but results in higher profits in future periods as

the asset isn't depreciated.

Effects on value of assets when capital expenditure incorrectly treated as revenue expenditure:

Asset Understatement: Assets are undervalued on the statement of financial position.

Depreciation: Lower depreciation expenses due to undervalued assets.

Example: "Star Ltd Co purchased office furniture for $5,000 and recorded it as revenue expenditure.

Explain the impact of this incorrect treatment on the financial statements."

Answer:

Impact on Profit:

Immediate:

Profit is understated by $5,000 because the expense was incorrectly

recorded on the income statement.Long-term: Depreciation expenses are understated in future periods,

leading to overstated profits in those periods.

Impact on Asset Valuation:

Understatement: Office furniture is not recorded as an asset, leading to a $5,000 undervaluation on the statement of financial position.

Depreciation: The absence of depreciation for the furniture results

in inaccurate financial statements over time.

Effects on profit when revenue expenditure incorrectly treated as capital expenditure:

Immediate Impact: Understates expenses, overstates profit.

Long-term Impact:

Overstates asset values and depreciation expenses, leading to incorrect profit figures

in subsequent periods.

Effects on value of assets when revenue expenditure incorrectly treated as capital expenditure

Asset Overstatement: Assets are overvalued on the statement of financial position.

Depreciation: Higher depreciation expenses due to overvalued assets.

Example: "Star Ltd Co spent $10,000 on repairs for its machinery and recorded it as capital expenditure.

Explain the impact of this incorrect treatment on the financial statements."

Answer:

Impact on Profit:

Immediate: Profit is overstated by $10,000 because the expense was not deducted

from the income statement.Long-term: Depreciation expenses will be higher, affecting future profits.

Impact on Asset Valuation:

Overstatement: Machinery is overstated by $10,000 on the statement of financial position.

Depreciation: Higher depreciation will be recorded over the useful life of the machinery.

Past Paper Questions: