4.4 Irrecoverable debts and provision for doubtful debts

When a business sells its product or inventory on credit (not cash) then there is an understanding that some credit customers (debtors) might not pay and the business might not get the sales revenue. This estimation is set by the business as a percentage (Provision for Doubtful Debts) at the start of financial period. 🤔

During the financial year, some debtors don’t pay due to many reasons such as declaring bankruptcy, death or any other reason then a business knows this debt is irrecoverable from a debtor called irrecoverable debt (bad debts) which becomes an expense to the business. 😭

Finally the business needs to close the default debtor account which is called (write off) 🙁

Miracle happens in business too! 🤩

Once in a blue moon a previously default customer returns to the business with the intention to return the debt may be full or partial amount. This is good news for the business and accounting has some set rules to record this money. The business would not record or open previously closed customer account. It is Just simply recorded money received -cash or bank(Debit) and irrecoverable debt credit that was previously debited (cancel out effect). Statement of profit or loss would record it as income so increase profit for that period whereas current asset is increase with the same value

Next if a business wishes to continue dealing with the same customer then a new debtor account will be opened in future or if the business decides to deal only cash with the same customer.

Irrecoverable Debts and Recovery of Debts Written Off

Definition

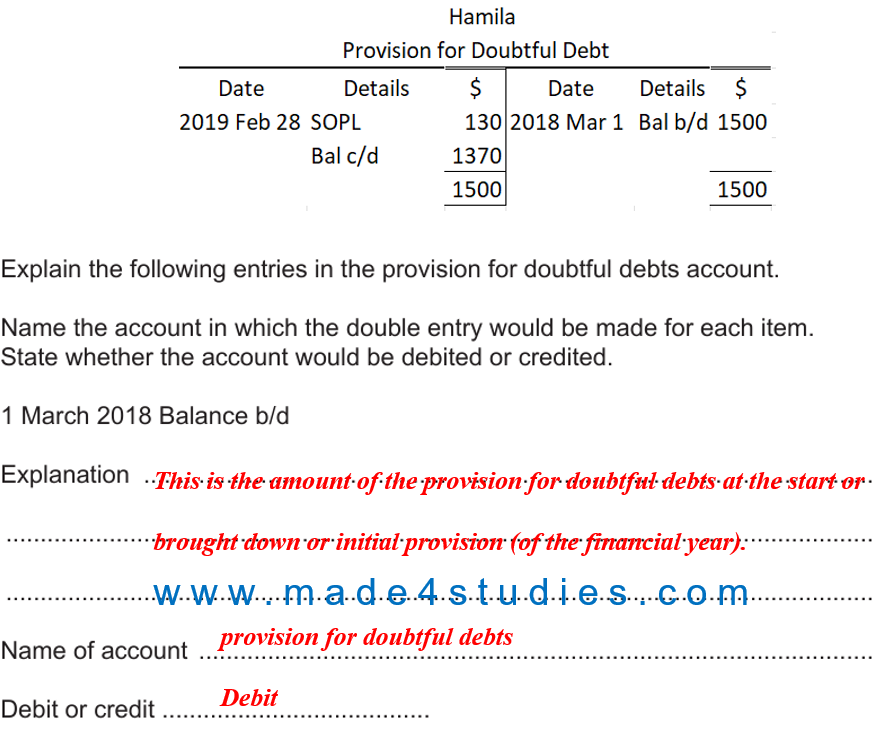

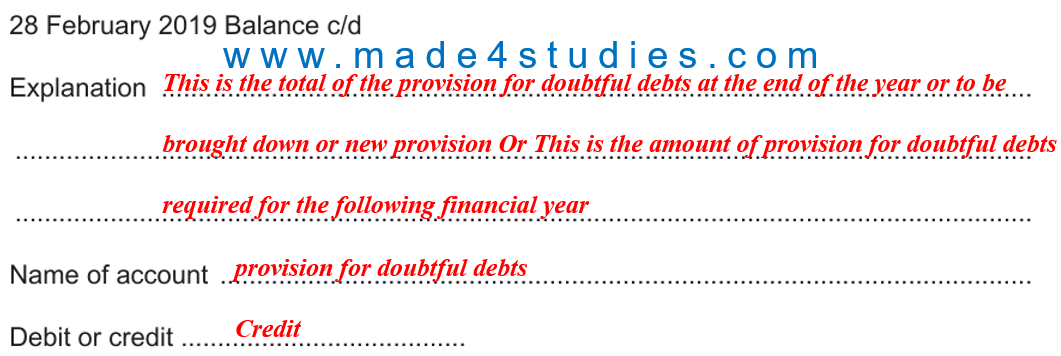

Provision for Doubtful Debts: An adjustment made to trade receivables based on an estimate of future irrecoverable debts. (It is also called as Allowance for Doubtful Debt or Bad debts)

Irrecoverable Debts: An amount owed to a business by a credit customer that cannot pay or will not pay the money that is owed. This amount is written off. (It is also called as Bad Debts Expense)

Recovery of Debts Written Off: When money is received in payment of a debt that has been previously written off. (It is also called as Bad Debts Recovered)

Provision for Doubtful Debts

Reasons for Maintaining a Provision for Doubtful Debts:

Anticipate potential losses from uncollectible receivables.

Present a more realistic view of the expected cash flow.

Comply with the prudence concept in accounting, ensuring that revenue is not overstated.

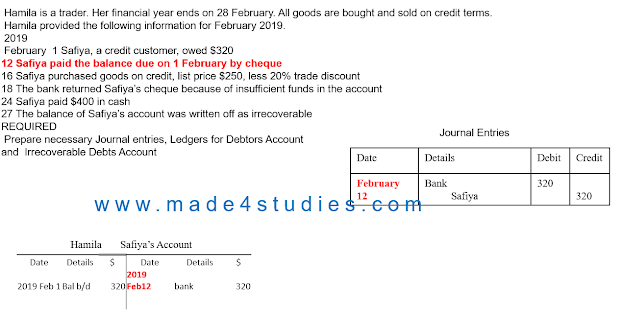

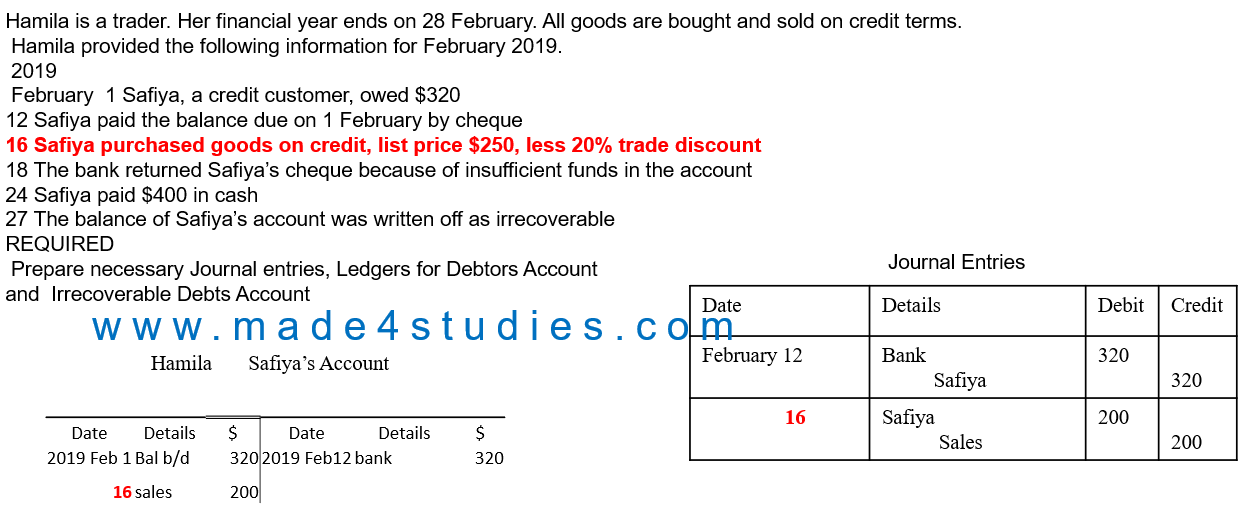

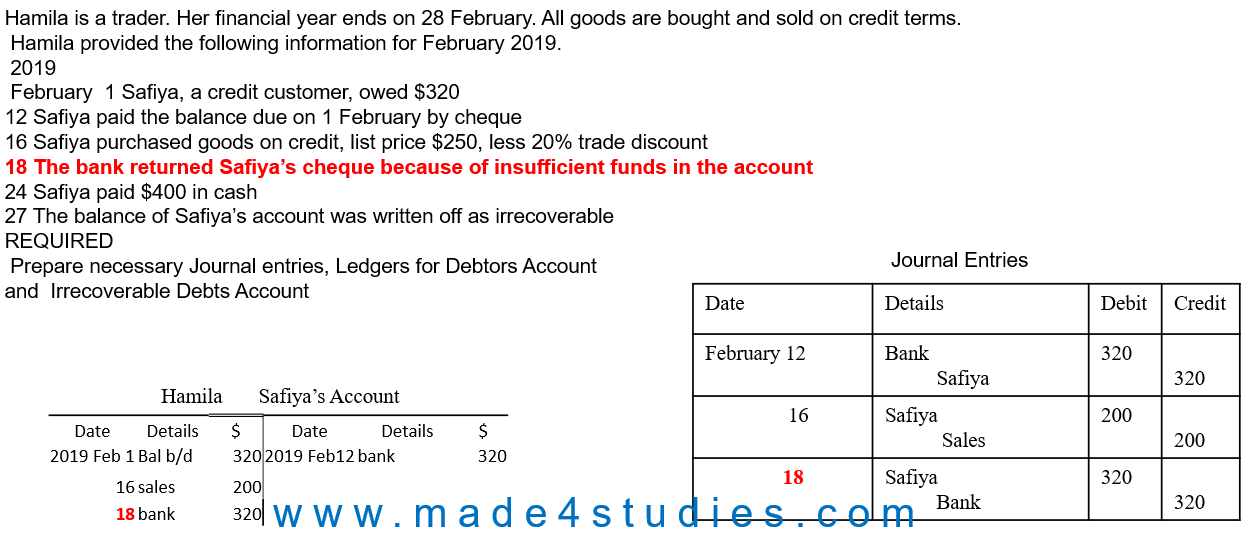

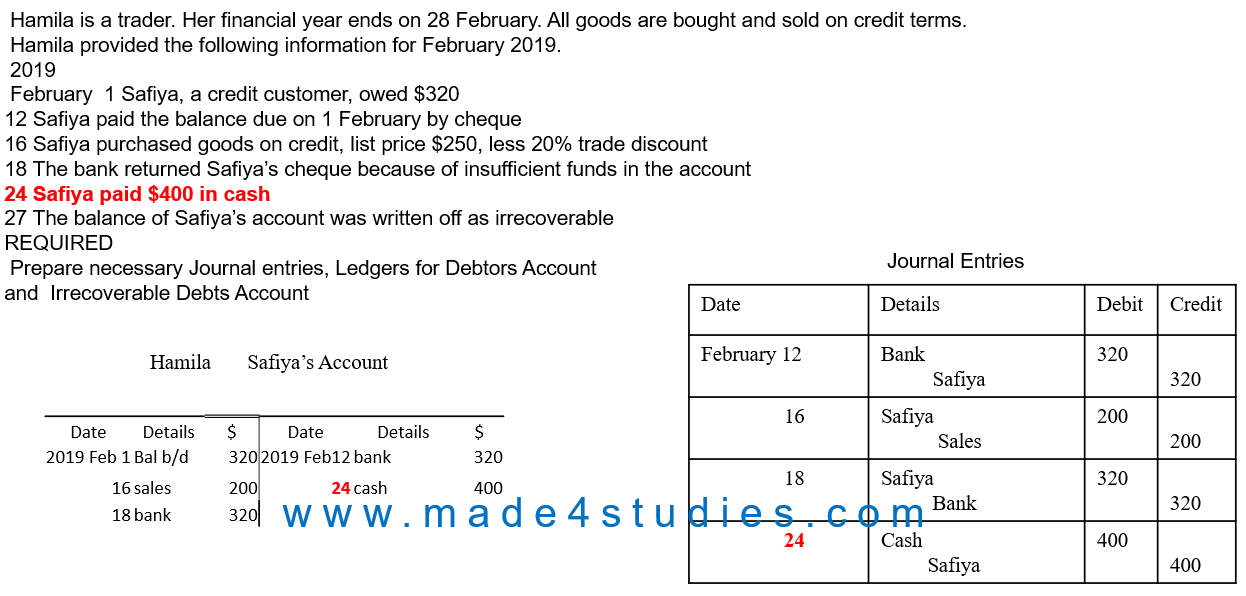

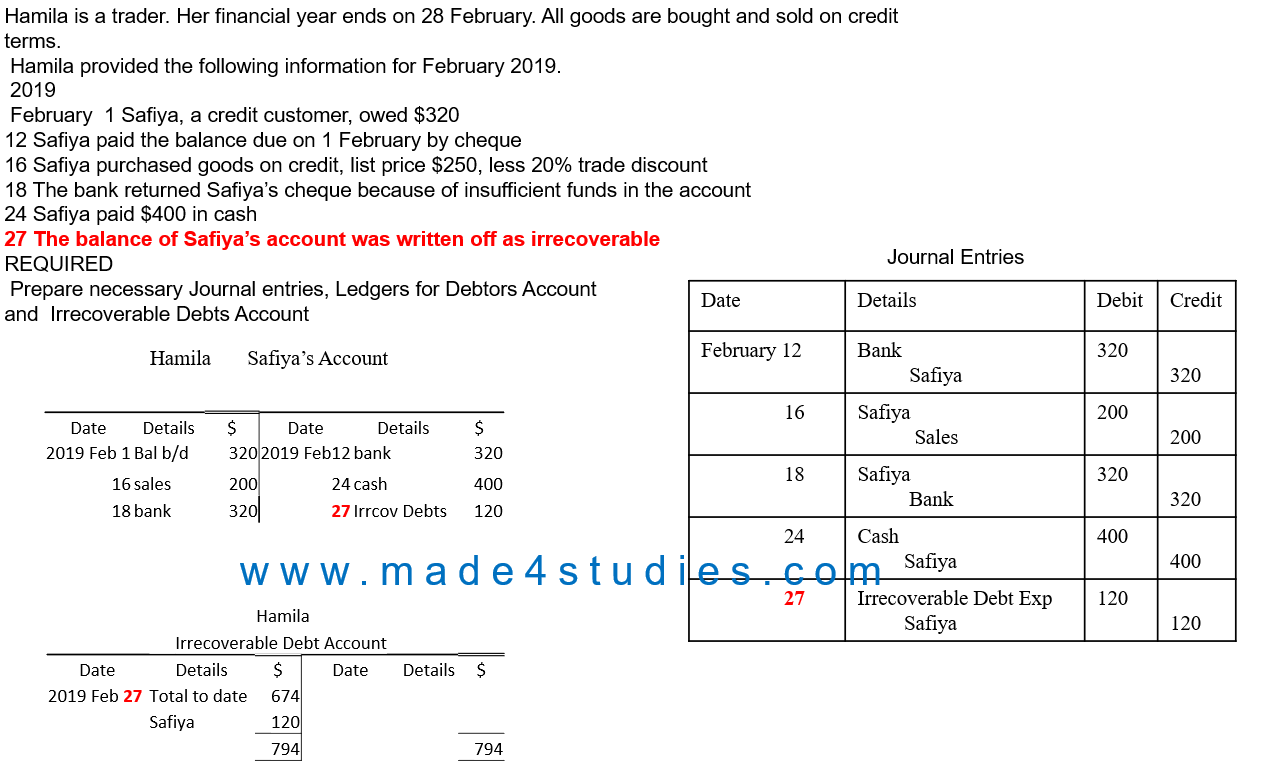

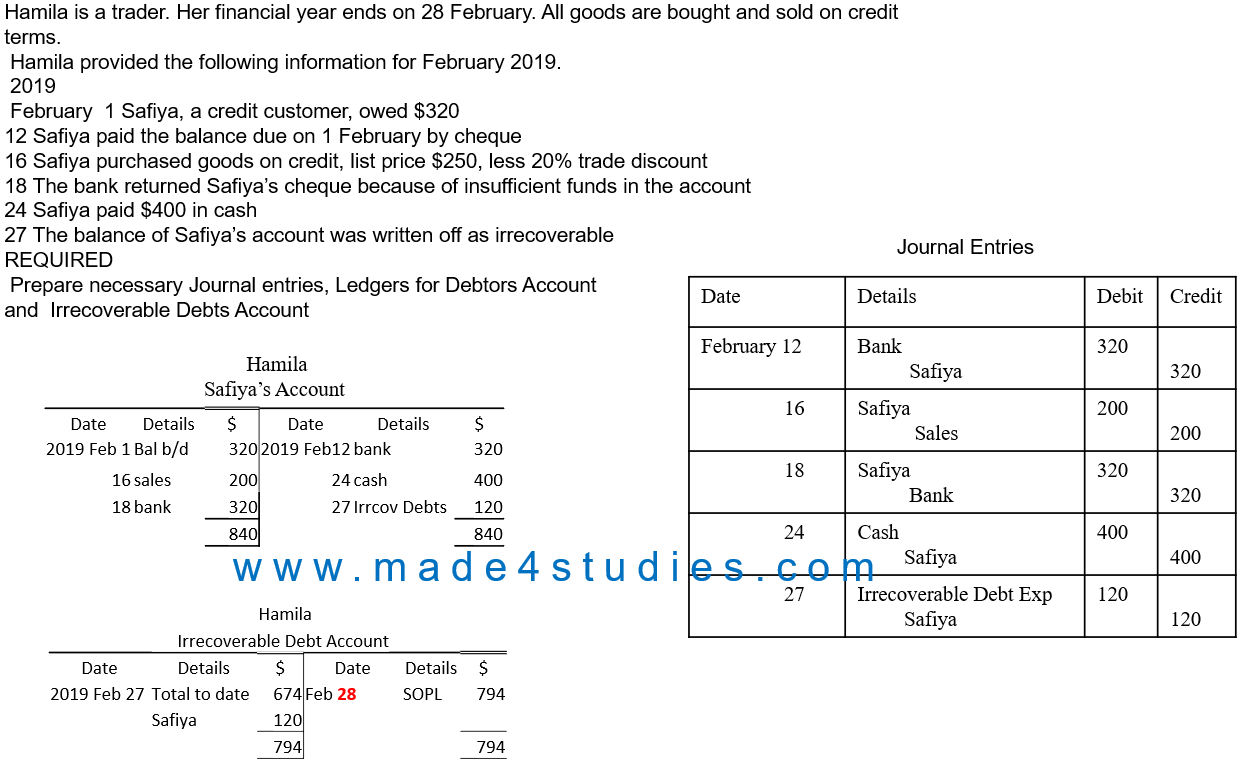

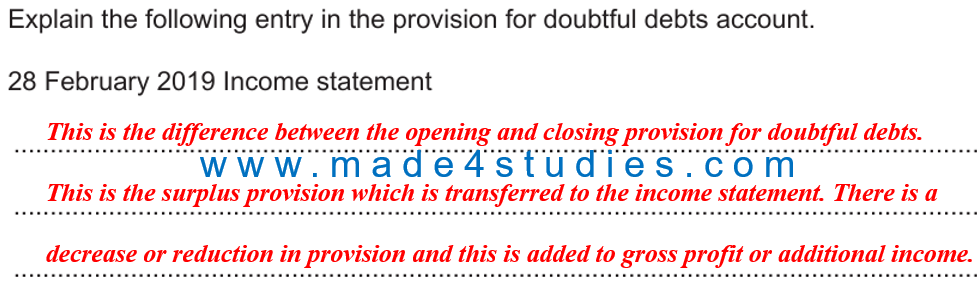

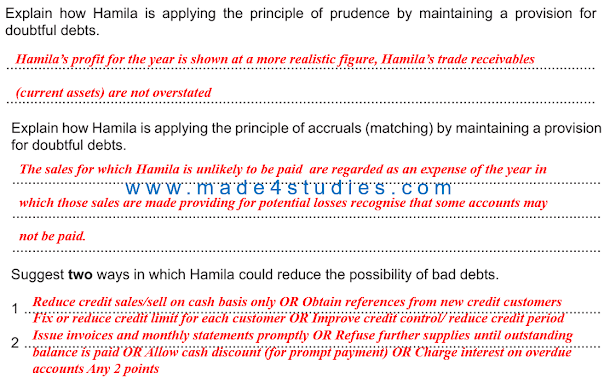

Past Paper Practice Question

Step by step solution: