2.3 Books of prime entry

Books of Prime Entry

Books of prime entry are specialized journals used to record specific types of transactions before they are posted to the general ledger. They streamline the recording process and provide efficient organization of accounting data.

Advantages of Using Various Books of Prime Entry

- Specialization: Each book is dedicated to a specific type of transaction, reducing errors and facilitating faster data entry.

- Efficiency: Entries can be made quickly as transactions occur, which helps in timely reporting and analysis.

- Division of Labor: Different staff members can manage different books, improving workflow and accountability.

- Detailed Analysis: Provides detailed records for specific types of transactions, aiding in financial analysis and decision-making.

Use of and Process Accounting Data in Books of Prime Entry

1. Cash Book

Records all cash transactions, including payments received and made.

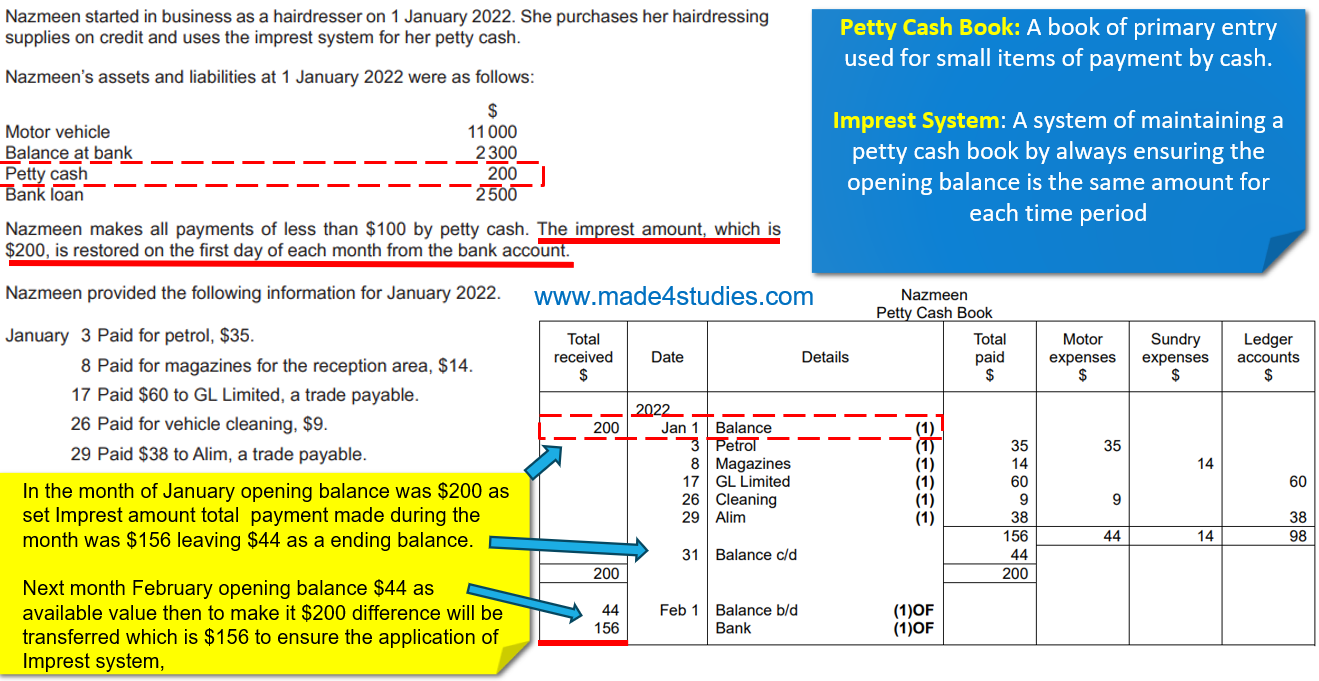

2. Petty Cash Book

Used to record small, routine expenses paid from petty cash.

Imprest System of Petty Cash

The Imprest system is used to manage petty cash efficiently:

Initial Fund: A fixed amount is placed in the petty cash float.

Replenishment: When the petty cash fund is low, it is replenished to its original amount.

Records: All petty cash transactions are recorded in the petty cash book to track expenditures.

3. Sales Journal (Sales Day Book)

Records credit sales made to customers.

4. Purchases Journal (Purchases Day Book)

Records credit purchases made from suppliers.

5. Sales Returns Journal (Returns Outwards Book)

Records goods returned by customers.

6. Purchases Returns Journal (Returns Inwards Book)

Records goods returned to suppliers.

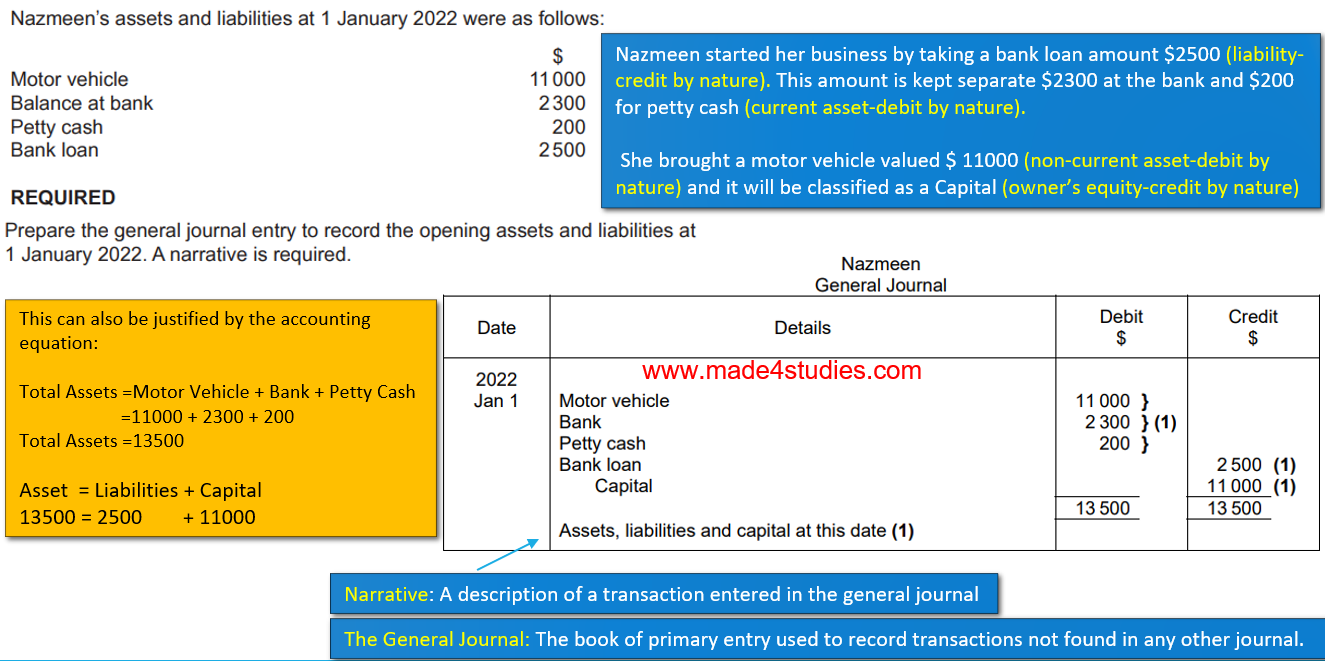

7. General Journal

The book of primary entry used to record transactions not found in any other journal.

Example

Posting Ledger Entries from Books of Prime Entry

Entries from books of prime entry are posted to the respective ledger accounts based on the double entry system.

For example, sales journal entries are posted to individual customer accounts in the sales ledger.

Distinguish Between and Account for Trade Discounts and Cash Discounts

- Trade Discount: Reduces the selling price of goods or services before an invoice is issued. Not recorded in the books; it's deducted directly from the sales invoice.

- Cash Discount: Offered to encourage early payment of invoices. Recorded in the books and accounts as a deduction from the amount owed by the customer.

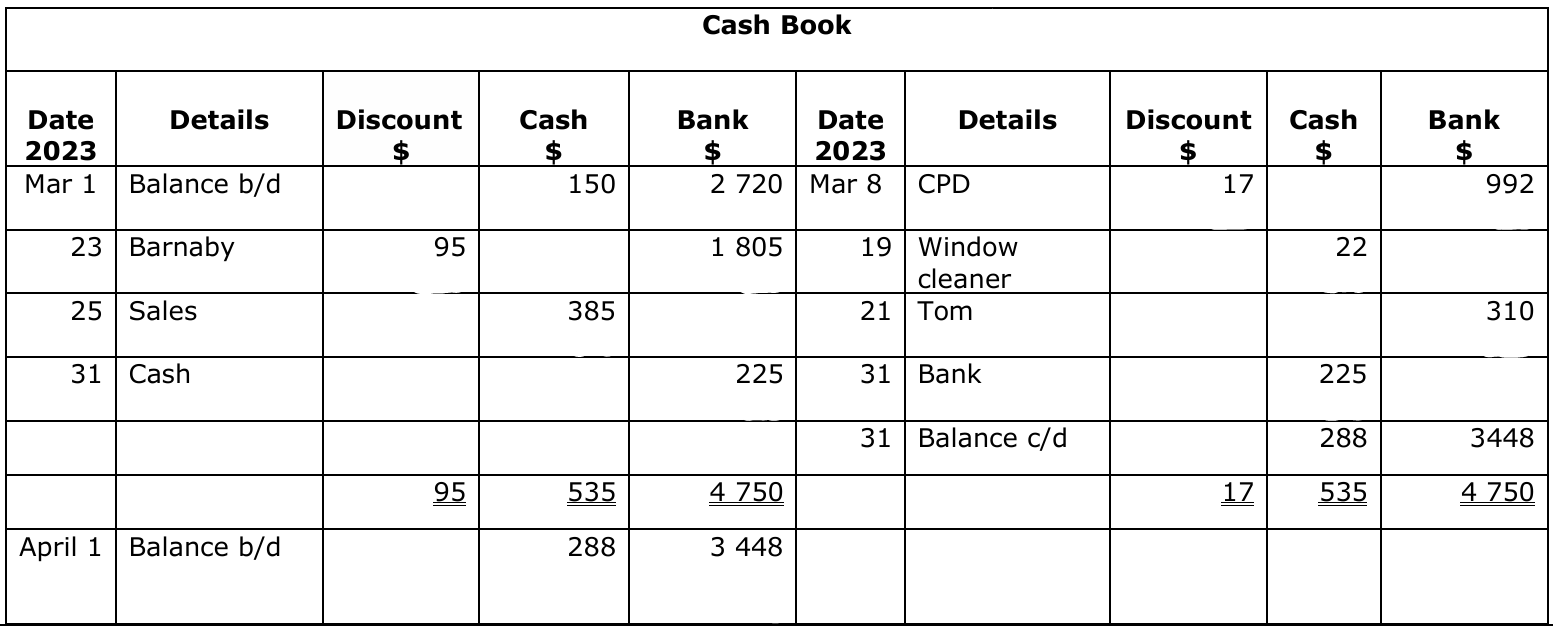

Dual Function of the Cash Book

The cash book serves two main purposes:

- Book of Prime Entry: Records all cash transactions.

- Ledger Account for Bank and Cash: Shows the balance of cash and bank accounts, summarizing all cash transactions.

Use of and Record Payments and Receipts Made by Bank Transfers and Other Electronic Means

Payments and receipts made by bank transfers or electronic means are recorded in the cash book as follows:

- Payments: Debited to the relevant expense or asset account.

- Receipts: Credited to the relevant income or asset account.