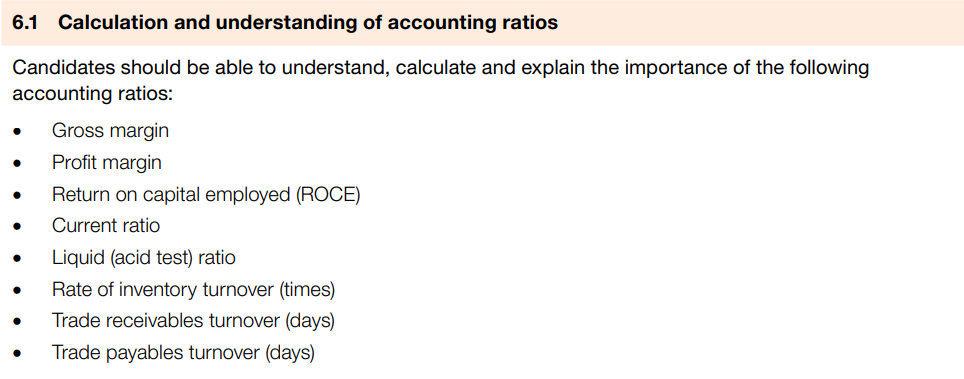

6.1 Calculation and understanding of accounting ratios

Accounting Ratios compares two key figures from the financial statement of a business to assess the financial performance of a business and to make comparisons over time and with the performance of other businesses.

For example, the current ratio compares the value of current assets to the current liabilities of a business to assess whether it will be able to settle its debts as they fall due

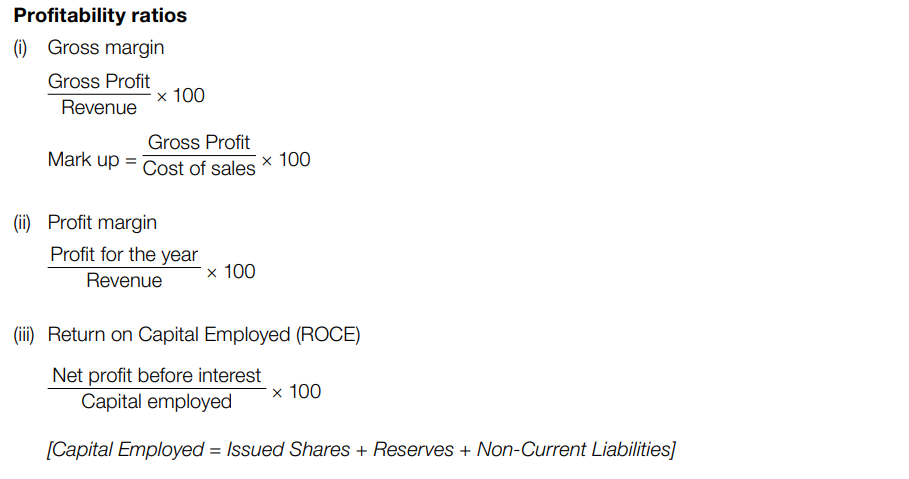

Profitability Ratios

Gross margin: The gross profit of a business expressed as a percentage of revenue generated by sales(revenue)

OR Gross margin measures the percentage of revenue that exceeds the cost of sales (COS). It indicates how efficiently a company produces and sells its goods.

Formula:

Gross Margin = Gross Profit×100

Sales (revenue)

Importance: It helps in assessing the profitability of a company's core activities, excluding overhead costs.

Benchmark: A typical gross margin for retail businesses might be around 20-50%. Higher margins indicate more efficient production processes.

Example: A company has sales of $200,000 and a gross profit of $60,000. Calculate the gross margin.

Gross Margin= 60,000×100=30%

200,000

Profit margin

The profit for the year of a business expressed as a percentage of revenue generated by sales.

OR

It is the percentage of revenue that remains as profit after all expenses have been deducted.

Formula:

Profit Margin= Profit for the year (Net Profit) ×100

Sales (revenue)

Importance: This ratio indicates the overall efficiency of a business in managing its expenses and generating profit.

Benchmark: A typical profit margin might range from 5-10% for many industries. Higher margins suggest better control over costs.

Example: If the Profit for the year (net profit) is $20,000 and the sales are $150,000, what is the profit margin?

Profit Margin= 20,000 ×100=13.33%

150,000

Return on Capital Employed (ROCE)

A measure of how well a business is using its assets to generate or ‘return’ a profit.

It expresses the profit for the year of a business as a percentage of the value of owner’s capital and loan capital invested in business assets (total assets less current liabilities)

OR

It measures the profitability and efficiency of capital investments in a business.

Formula:

ROCE = Profit for the year(Net Profit) x 100 (Sole Trader / Partnership)

Capital Employed

Capital Employed: Total Assets - Current Liabilities

ROCE = Profit before Interest and Tax (PBIT) x 100 (Limited Companies)

Capital Employed

Capital Employed: issued shares + reserves +non current liabilities

Importance: It shows how well a company is using its capital to generate profits.

Benchmark: A typical ROCE benchmark is around 10-15%. Higher values indicate more efficient use of capital.

Example 1: A business has a net profit before interest and tax of $50,000 and capital employed of $250,000. Calculate the ROCE.

ROCE= 50,000×100=20%

250,000

Example 2: A Limited company provided the following information on 30 December 2023.

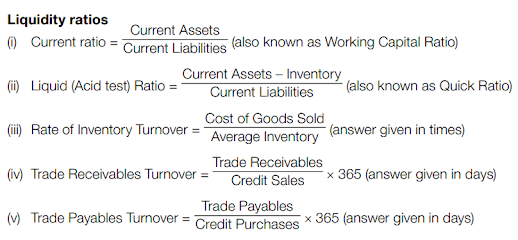

Liquidity Ratio

Liquidity: A measure of the ability of a business to pay its short-term debts

Current Ratio

Definition: The current ratio measures a company's ability to pay short-term obligations with its short-term assets.

OR

A measure of the ability of a business to settle its current liabilities from its current assets:

It compares the value of current assets to the value of current liabilities at a given point in time and is also known as the working capital ratio

Formula:

Current Ratio= Current Assets

Current Liabilities

Importance: A higher ratio indicates a stronger liquidity position.

Benchmark: A typical benchmark is around 1.5-2.0. Ratios below 1 indicate potential liquidity problems.

Example:

5. Liquid (Acid Test) Ratio

Definition: This ratio is a stricter measure of liquidity, excluding inventory from current assets.

OR

A measure of the ability of a business to quickly settle its current liabilities from its cash and other current assets without having to sell off any of its inventory of goods. Also known as the quick ratio

Formula:

Liquid Ratio (Acid Test)= Current Assets−Inventory

Current Liabilities

Importance: It shows a company's ability to meet short-term liabilities without relying on the sale of inventory.

Benchmark: A typical benchmark is around 1.0. Ratios below 1 suggest potential liquidity issues.

Example:

Activity or Efficiency Ratio

6. Rate of Inventory Turnover (Times)

This ratio indicates how often a business's inventory is sold and replaced over a period.

OR

The number of times during an accounting year a business ‘turns over’ (sells off and replaces) its inventory of goods for resale. It is calculated as the costs of sales divided by the average inventory held by the business during a given year . The higher the rate if turnover the more revenue a business will be earning, the less storage space it needs and the less working capital it will have tied up in inventory

Formula:

Rate of Inventory Turnover= Cost of Sales

Average Inventory

Importance: A higher turnover rate implies efficient inventory management.

Benchmark: A typical rate is around 5-10 times per year, depending on the industry.

Example:

Ekua is a trader who sells household furnishings. She has provided the following information.

7. Trade Receivables Turnover (Days)

This ratio measures the average number of days it takes a business to collect payment from its credit customers.

Formula:

Trade Receivables Turnover= Credit Sales ×365

Trade Receivables

Importance: It helps in understanding the effectiveness of the company’s credit policies and cash flow management.

Benchmark: A typical benchmark is around 30-60 days. Longer periods indicate potential cash flow issues.

Example:

8. Trade Payables Turnover (Days)

This ratio measures the average number of days it takes a business to pay its credit suppliers.

Formula:

Trade Payables Turnover= Credit Purchases ×365

Trade Payables

Importance: It provides insight into the company's payment policies and liquidity position.

Benchmark: A typical benchmark is around 30-60 days. Longer periods could indicate better credit terms from suppliers or liquidity issues.

Example: