5.2 Partnerships

Home

You will not be required to answer questions on the admission/departure of a partner, the dissolution of a partnership or changes to a profit sharing ratio.

Partnership: A business that is controlled by a minimum of two owners.

Advantages and disadvantages of forming a partnership

Partnership Agreement (deed of partnership)

It is an agreement that outlines the conditions that partners have consented to.

Importance and Contents of a Partnership Agreement

A partnership agreement is a legal document outlining the rights, responsibilities, and obligations of each partner. It is crucial to prevent disputes and ensure smooth operation.

Contents of a Partnership Agreement:

Capital Contributions: Amount each partner invests in the business.

Profit and Loss Sharing: How profits and losses are distributed among partners.

Responsibilities: Specific roles and duties of each partner.

Decision Making: Procedures for making business decisions.

Dispute Resolution: Methods for resolving conflicts.

Dissolution: Conditions under which the partnership may be dissolved.

What are the rules when there is no partnership agreement?

The accounting section of the Partnership Act 1890 applies

Profits and losses are to be shared equally.

There is to be no interest allowed on equity.

No interest is to be charged on drawings.

Salaries are not allowed.

If a partner puts a sum of money into the business in excess of the capital he or she has agreed to subscribe, that partner is entitled to interest on this advance at the rate of 5% per annum.

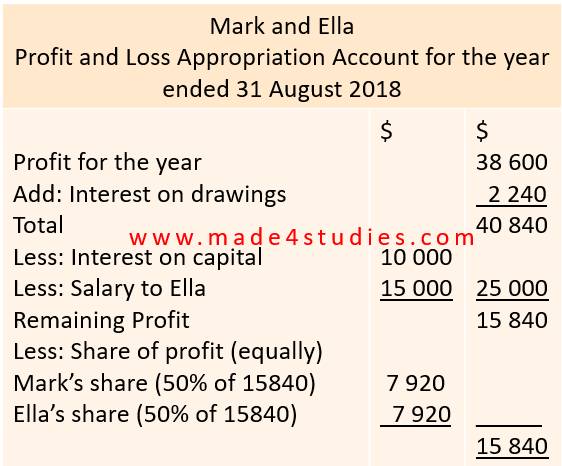

Appropriation Account

Definition: An account that shows how a partnership’s profit or loss for the year is shared out between partners

OR

The part of the statement of profit of loss that records the distribution of the profit to the partners.

Purpose of an Appropriation Account

An appropriation account is part of the financial statements of a partnership. It shows how the profit or loss of the business is divided among the partners after accounting for interest on capital, interest on drawings, and partners’ salaries.

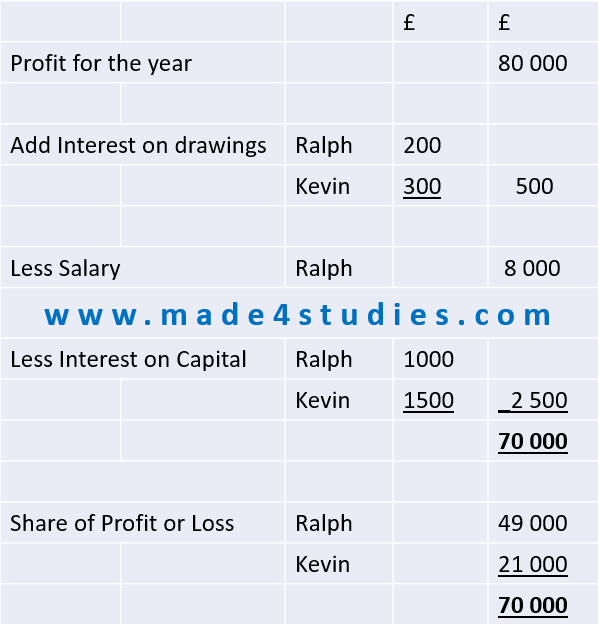

Example

Two partners: Ralph and Kevin. Their profit for the year is £80 000.

Interest on drawings: Some partnership agreements state that partners should be charged interest on any money taken out of the business during the year. This is to demotivate partners from taking too much cash out of the business.

In this example, Ralph took drawings of £2000 and Kevin withdrew £3000 from the business. Interest is charged at 10%.

Ralph: £2000 @ 10% = £200

Kevin: £3000 @ 10% = £300

Partnership salaries: Some partners may work in the business, whereas other partners may simply invest in the business without being involved in the running of the business. Partners who work in the business may be entitled to a salary.

In this example, Ralph is paid an annual salary of £8000.

Interest on capital: This is paid on the individual capital invested in the business by each partner.

In the exam, you will normally be expected to calculate this. Ralph and Kevin have capital of £20000 and £30000 respectively. Interest on capital is 5%.

Ralph: £20 000 @5% = £1000

Kevin: £30000@ 5% = £1500

Share of profits: This will involve another calculation and the ratio will be given in the exam. The ratio will normally reflect the workload of the partners or the amount of capital that has been invested.

Ralph and Kevin share profits on a 7:3 ratio.

£70000 / 10 (7 + 3) = £7000

Ralph: 7 x £7000 = £49 000

Kevin: 3 x £7000 = £21 000

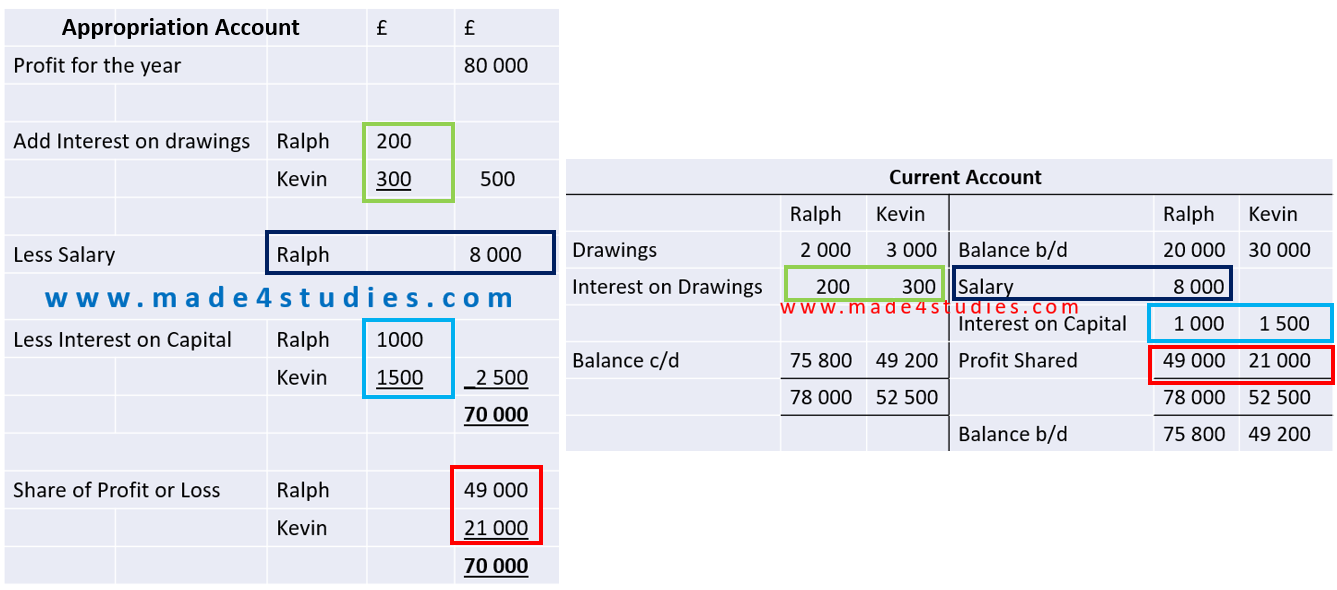

The appropriation account for Ralph and Kevin's partnership is shown below:

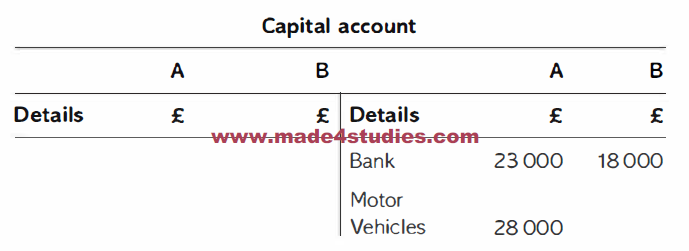

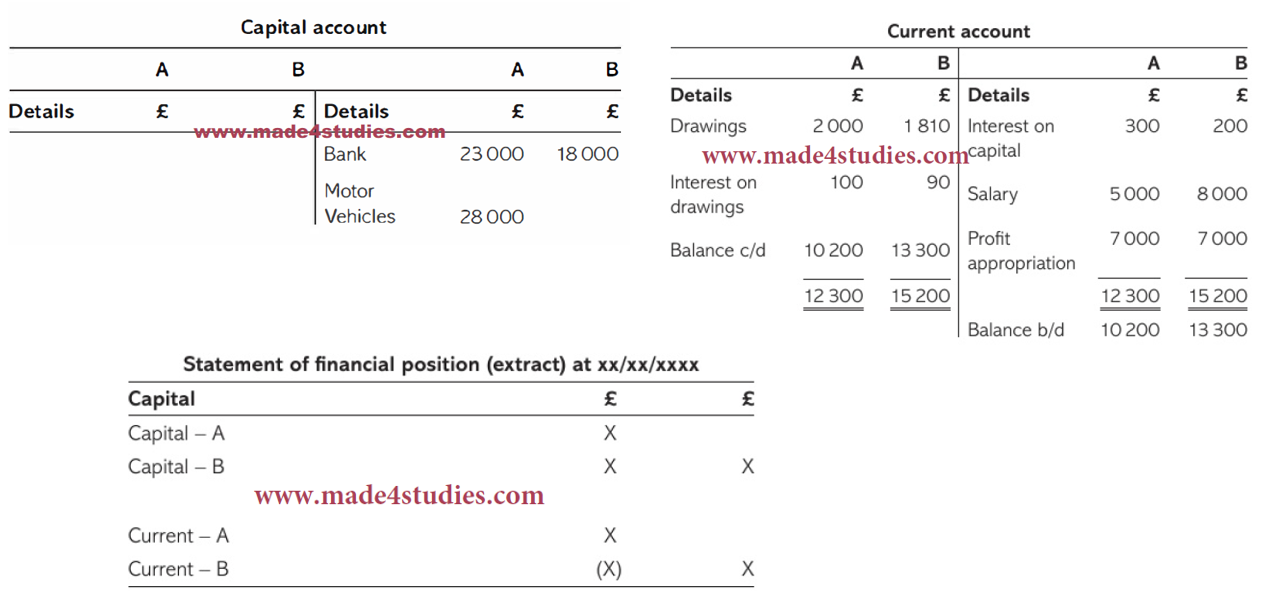

Capital Account

Definition:

fixed capital account when only capital transactions are recorded in the account

fluctuating capital account where all partners' transactions are entered in a single account

Explanation: The capital account is normally fixed, and only alters or changes when there is a permanent increase or decrease in the capital contributed by a partner.

For example: Partners A and B respectively contributed £23 000 and £18 000 cash into the business. The cash had been paid into the bank. Furthermore, Partner A contributed a motor vehicle with a valuation of £28 000 into the business.

Capital Account Ledger:

Current Account an account showing the movement of partners' drawings, interest on drawings and capital, salaries and share of profit/loss

The current account will show

the profits

interest on capital

salaries to which the partner may be entitled.

The drawings and any interest on drawings are debited to this account.

The balance of the current account at the end of each financial year represents the amount of undrawn (or withdrawn) profits. A credit balance will be undrawn profits, while a debit balance will be drawings in excess of the profits to which the partner is entitled.

It is possible to have a negative current account balance(in this case, Partner B’s current account) if the amount of drawings is more than the amount of profit received.

Are there any advantages of maintaining both a capital account and a current account for each partner?

Yes,

Easier to see amount invested by each partner

Easier to calculate interest on capital

Easier to see the profit retained by each partner

Easier to see if a partner is making excessive drawings

So, it’s better to prepare both Capital and Current Accounts

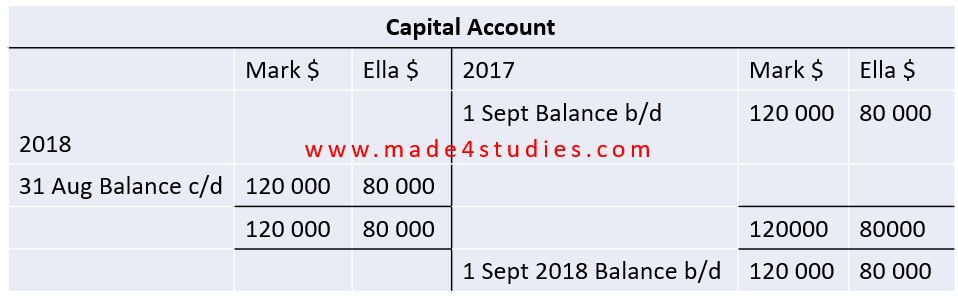

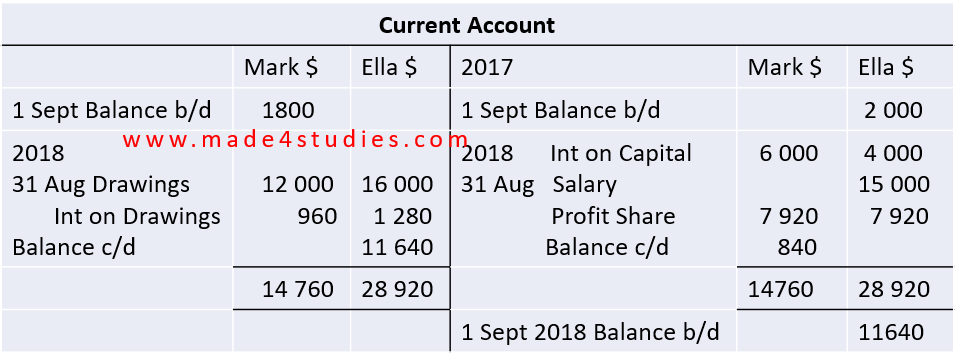

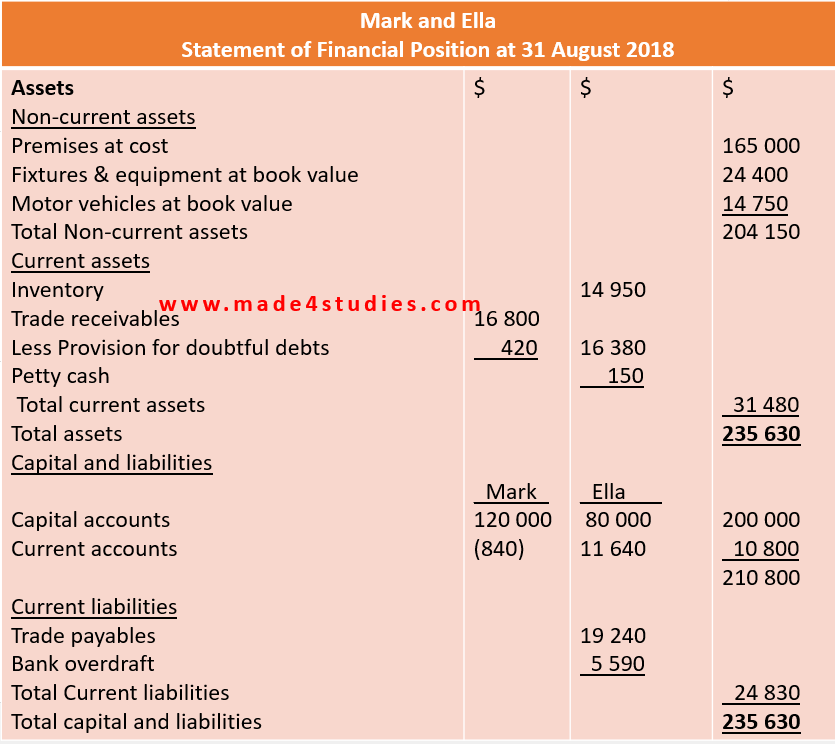

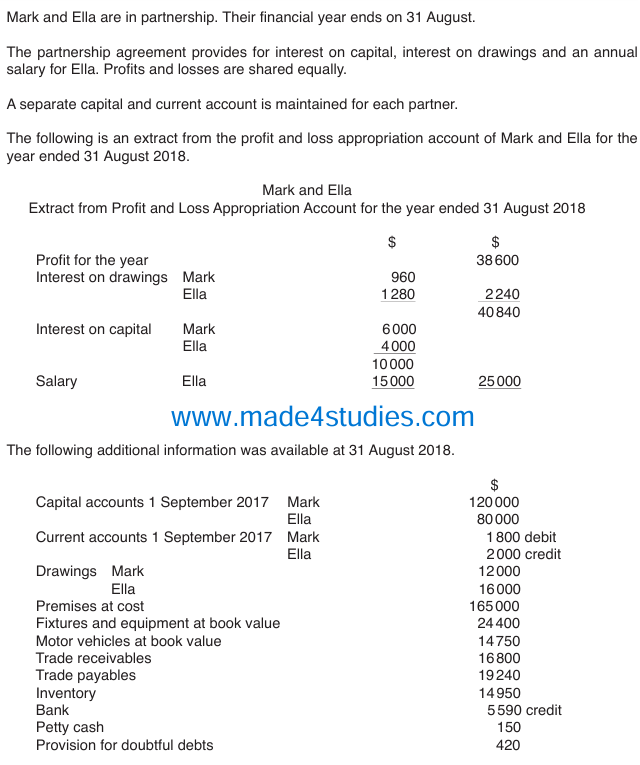

Past Paper Question

Prepare:

- Capital Account

- Current Account

- Appropriation Account

- Statement of Financial Position

Solution: